RAMmageddon 2026: Why Soaring Memory Prices Are Redefining PC Hardware

As of April 2026, building a PC has become a high-stakes financial balancing act. What analysts now call RAMmageddon, or “RAMpocalypse” for the more fatalistic, signals a turning point for the semiconductor industry. Unlike the 2020 chip shortage, driven by pandemic-induced disruptions, this crisis is rooted in a deeper structural shift.

I. Introduction: From Logistics Shock to Structural Mutation

We are no longer facing a simple inventory shortage; we are witnessing a massive reallocation of value. Since 2024, memory titans Samsung, SK Hynix, and Micron have executed an unprecedented strategic pivot. Following a market slowdown in 2023, these manufacturers capitalized on the artificial intelligence explosion to radically transform their production models.

This 2026 RAM shortage is not the result of idle factories, but of factories that have “chosen a side.” By diverting production capacities away from consumer-grade products toward high-margin components for data centers, manufacturers have fueled intense pressure on the consumer supply chain. This shift follows a ruthless industrial logic: the impact of AI hardware is so significant that demand for compute infrastructure now overrides personal computing needs, causing RAM prices to skyrocket for the end user.

II. The Mechanics of RAMmageddon: Why AI is Devouring Memory

To grasp the magnitude of this crisis, one must look deep into the semiconductor fabs. The market isn’t merely lacking components; it is undergoing a technical metamorphosis dictated by profitability.

A. The Manufacturer’s Trade-off: DRAM vs. HBM

The system memory you install in your PC (DDR4 or DDR5) and the memory powering AI models (HBM — High Bandwidth Memory) share the same physical foundation, but their architectures differ radically. HBM stacks memory layers vertically to achieve the colossal transfer speeds essential for processing the billions of parameters in modern LLMs.

However, HBM production is highly resource-intensive: it requires significantly more wafer capacity than conventional DRAM for an equivalent memory output due to its complex 3D stacking and packaging. Faced with substantially higher margins in the enterprise segment, manufacturers have made a rational trade-off: reducing consumer DDR output to prioritize HBM and data center-grade memory.

This shift directly exacerbates the global AI infrastructure bottleneck, as modern accelerators depend on ultra-high-bandwidth memory to operate efficiently.

B. Project Stargate and the Insatiable Appetite of Data Centers

The scale of this imbalance is best illustrated by pharaonic initiatives. Analysts from TrendForce and Tom’s Hardware estimate that projects like OpenAI’s Project Stargate could monopolize a staggering share of global supply.

While initial analyst projections suggested that OpenAI and its partners could represent up to 40% of global memory production dedicated to AI (notably VRAM/HBM), the actual volumes ordered have been significantly lower. Nevertheless, these announcements played a decisive role by signaling massive future demand, triggering a broader gold rush among AI players — hyperscalers and startups alike — to secure available memory capacity.

This preemptive hoarding has contributed to generalized tension across the entire market, including standard PC RAM (DRAM). This crowding-out effect is particularly violent as hyperscalers like Google, Amazon, and Meta place “blank check” orders, accepting any price to secure their stocks. This pressure mechanically drives up the costs of the hardware stack and, by extension, the price of every single stick of system memory available for the rest of the world. We are no longer in a market of supply and demand, but in a priority-booking economy where the individual consumer is served last.

III. Collateral Damage: A Consumer Market Gasping for Air

The shift in industrial priorities toward AI isn’t just about abstract figures in financial reports; it is concretely redefining what we can buy and at what cost.

A. The Case of Micron and the End of Crucial: A Powerful Symbol

One of the most significant shocks of this RAMmageddon is undoubtedly Micron’s decision to drastically reduce its exposure to the consumer market.

In February 2026, Micron officially ceased shipments under its consumer-facing brand, Crucial, marking a strategic retreat from the consumer segment. While products remain available via existing inventory at certain retailers, no new production for the general public is currently guaranteed.

This strategic move, driven by the need to support “strategic clients” in high-growth sectors like AI, marks the end of an era for PC builders. For Micron, the message is clear: the “Consumer” segment no longer offers the necessary profitability compared to the appetite of data centers. This withdrawal leaves an immense void in the PC RAM market, forcing buyers toward alternatives that are often more expensive or harder to find.

B. From Dell to Raspberry Pi: The Disappearance of Entry-Level

The shockwave is propagating through the entire value chain. Major OEMs like Dell and HP have already warned that memory costs—which now represent up to 35% of the Bill of Materials (BOM) of a computer, compared to less than 20% previously—are leading to inevitable price hikes.

- Entry-level under threat: Gartner estimates that laptops under $500 are becoming an endangered species, as they are no longer economically viable to produce given current component prices.

- Low-cost hardware suffering: Even the education and hobbyist sectors are hit, with products like the Raspberry Pi facing price increases. This scarcity reinforces the necessity of exploring local-first AI alternatives that can run on existing, albeit limited, hardware.

- Bleak outlook: IDC analysts predict that this inventory pressure could lead to a significant drop in global PC and smartphone shipments throughout 2026.

In this climate, finding a laptop with 32GB of RAM at a decent price has moved from a standard shopping trip to a daily logistical challenge for the consumer.

IV. Software Optimization as a Lifeline?

Faced with this physical wall of silicon, the industry is looking for answers in the code. If the hardware is scarce, can software intelligence bridge the gap?

TurboQuant and the Subtle Signals of Efficiency

The announcement by Google of its TurboQuant technology on March 24, 2026, serves as a significant, albeit subtle, signal of hope. By claiming up to a six-fold reduction in memory consumption for local Large Language Models (LLMs), this compression technique points toward the possibility of doing more with less, although real-world impact remains to be validated.

However, nuance is required: while TurboQuant optimizes existing local deployments, it does not solve the physical demand for heavy infrastructure. This announcement sparked questions in the markets regarding future memory demand, with some investors anticipating that improved software efficiency might eventually cap the growth of hardware requirements. For those looking to optimize their current setups, choosing the best GPU for local AI remains critical to balancing VRAM capacity with these new architectural gains, especially when leveraging proprietary accelerators like Google’s TPU Trillium.

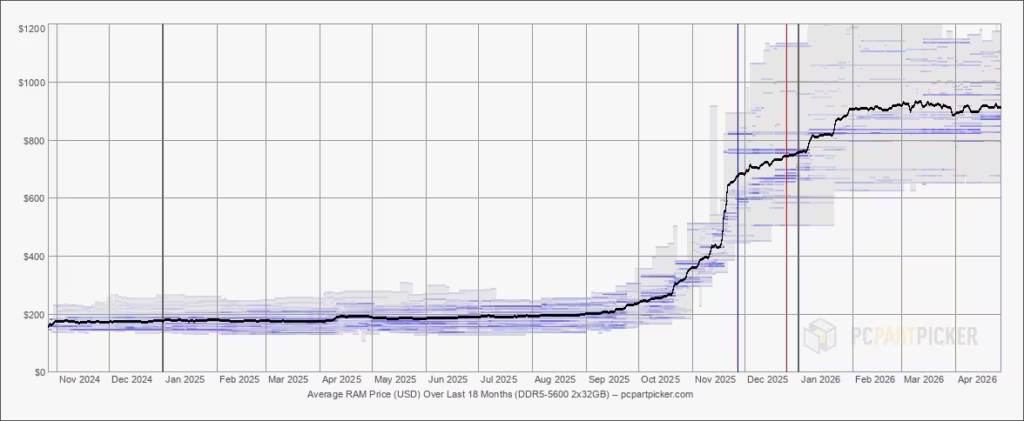

V. RAM Prices in 2027: Toward a Lasting “New Normal”

Perspectives for 2027 confirm that RAMmageddon is not a temporary glitch, but a durable market mutation.

Major analytical firms — including TrendForce, Counterpoint Research, and IDC — converge on a clear observation: no significant price correction is expected before late 2027. This persistent tension is driven by several structural factors:

- Skyrocketing AI demand, fueled by data centers and increasingly resource-heavy models.

- A supplier-led market, where manufacturers tightly control volumes to maximize profitability.

- The rise of HBM, which could represent up to 40–45% of the total memory market value by 2027.

In this context, even if minor price dips occur for DDR4 or DDR5, analysts agree that the market is entering a phase of structurally high pricing. The most likely scenario is not a return to the 2019–2022 price levels, but rather the emergence of a “new normal”, where system memory becomes a permanently expensive component in a PC’s budget.

VI. Conclusion: Toward a New Hardware Equilibrium

RAMmageddon is not merely a passing phase; it marks the end of the era of “disposable” and cheap components. In 2026, system memory has become the new oil of the digital economy, siphoned off as a priority by the wells of artificial intelligence.

As long as manufacturers like Samsung or SK Hynix continue to prioritize the record-breaking margins of HBM over consumer volume, the PC market must reinvent itself. Between radical software optimization and durably high prices, personal computing is entering a phase of forced sobriety. The question is no longer how much RAM you can afford to buy, but how your software will manage to survive with what remains.

VII. FAQ: Essential Facts About the 2026 RAM Shortage

Why is RAM so expensive in 2026?

Production has been massively diverted toward HBM (High Bandwidth Memory) for AI. This is significantly more profitable for chipmakers than the standard RAM used in our PCs.

Will RAM prices drop in 2027?

Analysts suggest that no significant price drop is expected until at least late 2027. The market is projected to remain tight with prices staying at a “new normal” high.

Is now the right time to buy memory?

According to IDC, the shortage could persist well into 2027. Waiting for a significant short-term price drop is considered a risky strategy in the current climate.

How does AI affect my computing budget?

The monopolization of resources by data centers drives up component costs. This directly impacts the cost of operating AI agents and the final retail price of all computer hardware.

Your comments enrich our articles, so don’t hesitate to share your thoughts! Sharing on social media helps us a lot. Thank you for your support!